Importing CSV Data

Supported Formats

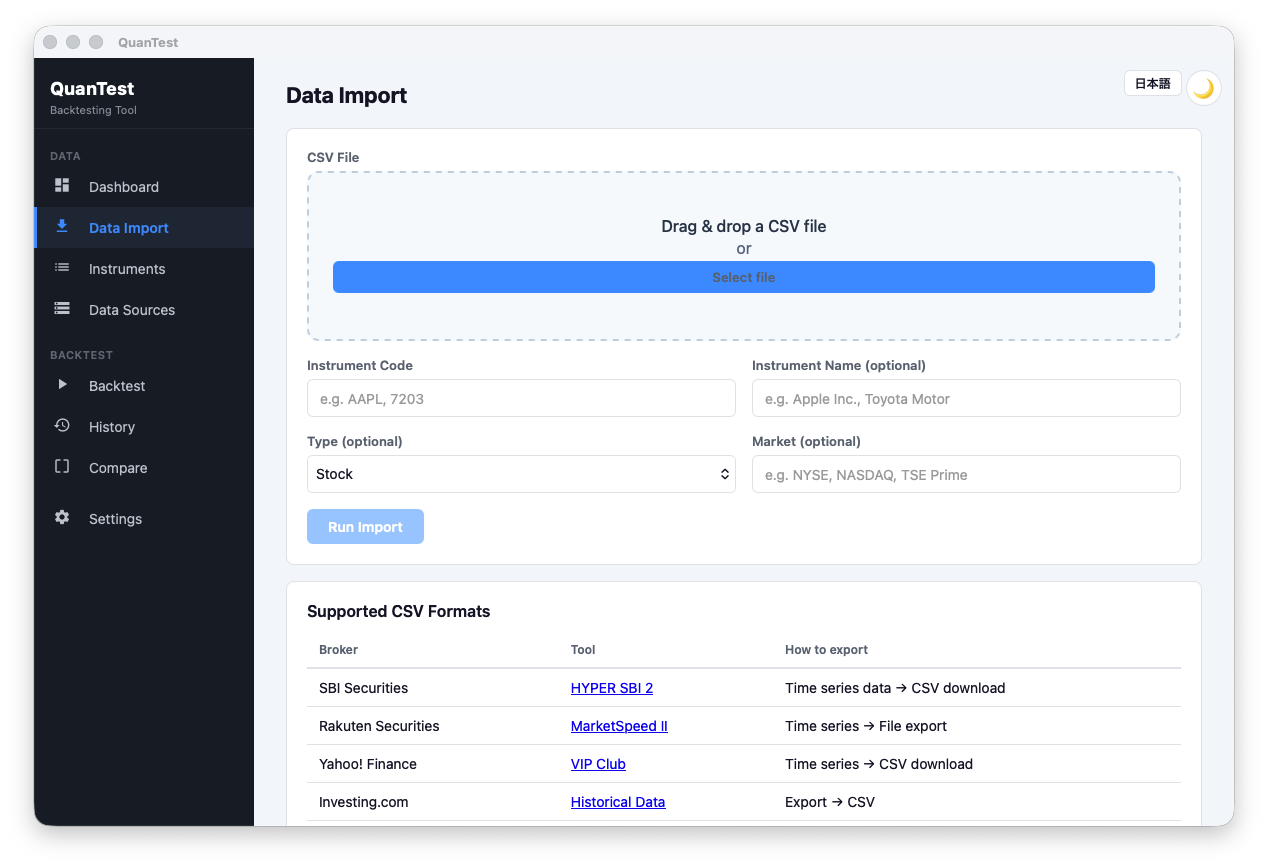

QuanTest supports the following CSV formats out of the box.

| Data Source | Where to Download |

|---|---|

| SBI Securities (HYPER SBI 2) | Instrument page → Chart → Historical Data |

| Rakuten Securities (MarketSpeed II) | Instrument info → Chart → CSV Download |

| Yahoo! JAPAN Finance (VIP Club) | Price History → CSV Download |

| Investing.com | Instrument page → Historical Data → Download CSV |

| Yahoo Finance (US) | Instrument page → Historical Data → Download |

| Custom CSV | Any CSV (column mapping required) |

Import Steps

1. Open the Data Import screen

Click “Data Import” in the left menu.

2. Select your CSV file

Drag & drop the CSV file onto the drop zone in the center of the screen, or click “Select File” to browse.

3. Enter instrument information

| Field | Description |

|---|---|

| Ticker | e.g., 7203 (Toyota Motor). Required. |

| Name | Optional. Displayed as the ticker if left blank. |

| Type | Select from: Stock / ETF / REIT / Other. |

| Market | Select from: TSE Prime / Standard / Growth / US, etc. |

4. Confirm the format

QuanTest reads the CSV headers and automatically detects the format. If successful, it shows something like “Format: SBI Securities HYPER SBI 2”.

If the format cannot be detected (Custom CSV): A column mapping panel appears. Map each column to Date, Open, High, Low, Close, and Volume.

5. Run the import

Click “Import”. A diagnostics panel appears when complete.

Reading the Diagnostics Panel

| Field | Description |

|---|---|

| Detected format | The CSV format that was identified |

| Estimated market | The market auto-detected from the data |

| Date range | Start and end dates of the imported data |

| Bar count | Number of trading days imported |

| OHLC integrity | Validates that High ≥ Open, Close, Low |

If everything looks good, click “Set Up Backtest” to go directly to the backtest configuration screen.

Notes

- Re-importing the same ticker appends new data rather than overwriting (duplicates are removed automatically).

- Too little data may prevent some strategies from running. At least 1–3 years of data is generally recommended.